A hedge is not a prediction that the market will fall. It is a deliberate trade that reduces a specific risk already inside a portfolio. The correct hedge begins with three questions: what risk are you trying to reduce, how much of it do you own, and what are you willing to pay to reduce it?

Portfolio value is not the same as market exposure. A $100,000 portfolio with a beta of 1.25 carries roughly $125,000 of market-equivalent exposure. Hedging $20,000 because it “feels like 20%” does not hedge 20% of that risk. Institutional investors size the hedge against beta-adjusted exposure, factor exposure, volatility, or a defined drawdown objective.

Every hedge has a cost. A short index position sacrifices upside. A protective put charges premium and loses value with time. A collar finances protection by capping gains. Futures are efficient but leveraged. Inverse ETFs are accessible but many reset daily and can drift from the intended inverse return over longer holding periods.

The best hedge is usually partial and governed by rules. Most investors do not need a permanently market-neutral portfolio. They need a repeatable policy that defines when protection is added, how large it becomes, what instrument is allowed, and when it is removed.

Hedging Is Risk Transfer, Not Panic Selling

Most newer investors meet hedging at exactly the wrong moment: after the market has already fallen, volatility has surged, and fear has replaced planning.

That is not hedging. That is emergency reaction.

A hedge is a position designed to offset a measurable risk in another position. If a portfolio is heavily exposed to the broad equity market, an index hedge can reduce market risk. If it is concentrated in semiconductors, a broad-market hedge may leave much of that sector risk untouched. If the concern is a single earnings event, hedging the entire portfolio may be wasteful.

The objective is not to make every loss impossible. That would usually require selling the portfolio or purchasing so much protection that the portfolio’s expected return disappears. The objective is to make an adverse outcome survivable.

This distinction matters:

Diversification spreads risk across assets whose returns are not perfectly correlated.

Position reduction removes exposure outright.

Hedging keeps the underlying investment while adding an offsetting exposure.

Insurance is a form of hedging with an asymmetric payoff: a known cost is paid to limit an unwanted outcome.

Before buying any hedge, an investor should be able to complete this sentence:

“I am protecting against _ for approximately _, and I will remove or rebalance the hedge when ____.”

If those blanks cannot be filled, the trade is probably an opinion, not a hedge.

Alpha and Beta: What Are You Actually Trying to Protect?

Institutional portfolio construction separates returns into two broad ideas: beta and alpha.

Beta is systematic exposure. It measures how sensitively an investment has moved relative to a chosen benchmark. A beta of 1.00 suggests that a portfolio has historically moved roughly in line with that benchmark. A beta of 1.25 suggests approximately 1.25% of movement for each 1% benchmark move, on average. Beta below 1.00 implies lower sensitivity; negative beta implies movement in the opposite direction.

The benchmark matters. A technology portfolio may show one beta to the S&P 500, another to the Nasdaq-100, and another to a semiconductor index. A statistically tidy hedge against the wrong benchmark can still be economically useless.

Alpha is the return not explained by the modeled benchmark exposure. In simplified terms, it is the residual return after accounting for market sensitivity. Investors often think of alpha as skill, security selection, timing, or differentiated insight. But measured alpha can also contain noise, omitted risk factors, stale relationships, and benchmark error.

The important insight is this: a good hedge removes unwanted beta while preserving as much intended alpha as possible.

Imagine an investor owns a group of companies because they believe those businesses will outperform. If they sell everything whenever the market weakens, they remove both the broad market exposure and the company-specific opportunity. A carefully selected index hedge can reduce some broad beta while leaving the long positions intact.

The CFA Institute describes systematic risk as market-wide risk that cannot be diversified away, while nonsystematic risk is local and may be reduced through diversification. That is the conceptual foundation of beta hedging.

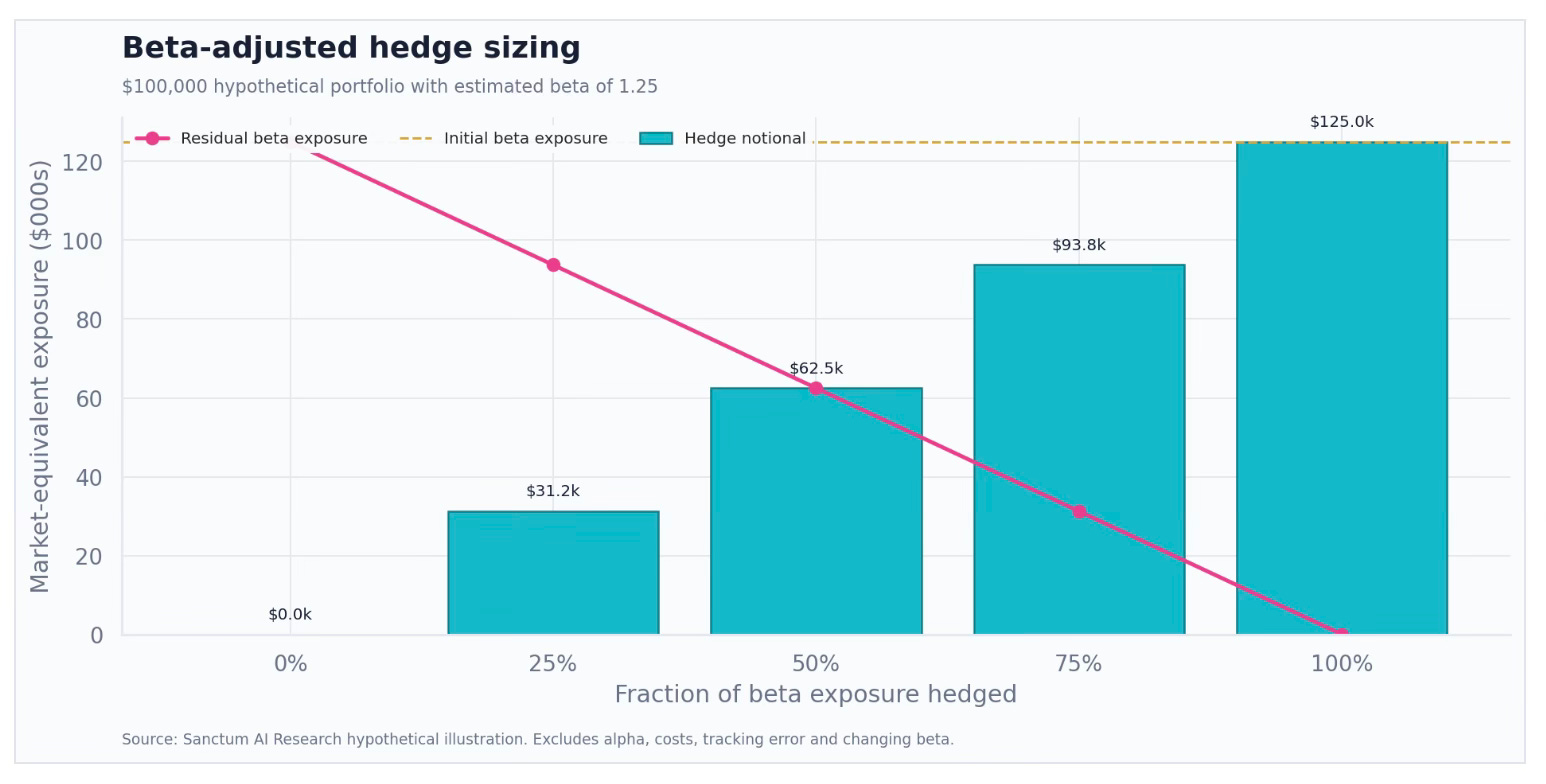

The First Institutional Method: Beta-Adjusted Notional

The simplest professional framework begins with a portfolio’s market value and estimated beta.

Beta-adjusted exposure = Portfolio value × Portfolio beta

Suppose a fictional growth portfolio is worth $100,000 and has an estimated beta of 1.25 to a relevant growth index.

Its beta-adjusted market exposure is:

$100,000 × 1.25 = $125,000

A full beta hedge would require approximately $125,000 of opposite index exposure. But a full hedge is rarely the desired outcome. It attempts to neutralize broad market sensitivity and may leave the portfolio dominated by stock-specific risk, basis risk, financing costs, and estimation error.

For a 50% beta hedge:

Hedge notional = $100,000 × 1.25 × 50% = $62,500

For a 25% beta hedge:

Hedge notional = $100,000 × 1.25 × 25% = $31,250

The percentage being hedged applies to beta-adjusted exposure, not simply portfolio value. All figures are hypothetical and exclude alpha, basis risk, costs, and changing beta.

If the hedge instrument itself has a beta materially different from 1.00 to the chosen benchmark, the notional must be adjusted again:

This is the first place many retail hedges fail: investors choose a convenient round-dollar short without measuring the exposure it is supposed to offset.

The Second Method: Minimum-Variance Hedging

Beta hedging asks, “How much benchmark exposure does the portfolio have?” Minimum-variance hedging asks, “What hedge ratio would have minimized the variance of the combined position?”

For one hedge instrument, the classical minimum-variance hedge ratio is:

This is mathematically similar to a regression coefficient. With multiple hedge instruments, institutions often estimate a multivariate regression or use a covariance matrix and optimizer. A technology portfolio, for example, might be modeled with broad-market, growth, semiconductor, size, and momentum factors.

This method can be powerful because portfolios rarely carry only one kind of beta. It can also produce deceptively precise answers.

Three warnings matter:

The hedge is backward-looking. Correlations and betas can change when the market regime changes.

A minimum-variance portfolio is not automatically a maximum-return portfolio. The optimizer may neutralize exposures the investor intentionally owns.

Unconstrained optimization can produce extreme positions. Institutions apply limits for gross exposure, liquidity, turnover, borrow availability, and concentration.

The practical answer is often a constrained hedge: use the model to understand risk, then cap the hedge at a level consistent with the mandate.

The Third Method: Target Volatility and Risk Budgets

Some institutions do not begin with hedge percentage at all. They begin with a target level of portfolio volatility.

If a portfolio’s expected annualized volatility rises from 15% to 25%, a volatility-targeting process may reduce net exposure or add hedges until expected volatility returns toward the target. A simplified exposure multiplier is:

If target volatility is 15% and estimated volatility is 25%, the simplified multiplier is 0.60. That suggests carrying roughly 60% of the previous risk, subject to portfolio constraints.

Volatility targeting is useful because the same dollar position can carry radically different risk in calm and turbulent markets. Its weakness is procyclicality: volatility often rises after prices have already fallen, so a purely mechanical process can force investors to de-risk late and re-risk after calm returns.

Institutions therefore blend volatility with other controls:

maximum gross and net exposure;

drawdown thresholds;

liquidity and days-to-exit limits;

concentration by sector, factor, or issuer;

Value at Risk and Expected Shortfall;

stress tests using historical and hypothetical shocks.

VaR, Expected Shortfall, and Drawdown: Three Different Questions

No single risk statistic defines the correct hedge.

Value at Risk (VaR) estimates a loss threshold over a specified horizon and confidence level. A one-day 95% VaR of $2,000 means the model expects losses to exceed $2,000 on roughly 5% of days, subject to its assumptions. VaR does not say how severe those worse outcomes may be.

Expected Shortfall, also called Conditional VaR, estimates the average loss within that tail beyond the VaR threshold. It is often more informative for hedge design because hedges are purchased for bad outcomes, not average days.

Maximum drawdown measures the decline from a prior peak to a subsequent trough. Investors experience drawdown directly, but historical maximum drawdown is sample-dependent and does not predict the next crisis.

A serious hedge review asks all three:

How much normal volatility should we tolerate?

What happens in the tail?

How much peak-to-trough damage can the strategy survive before behavior or mandate forces a sale?

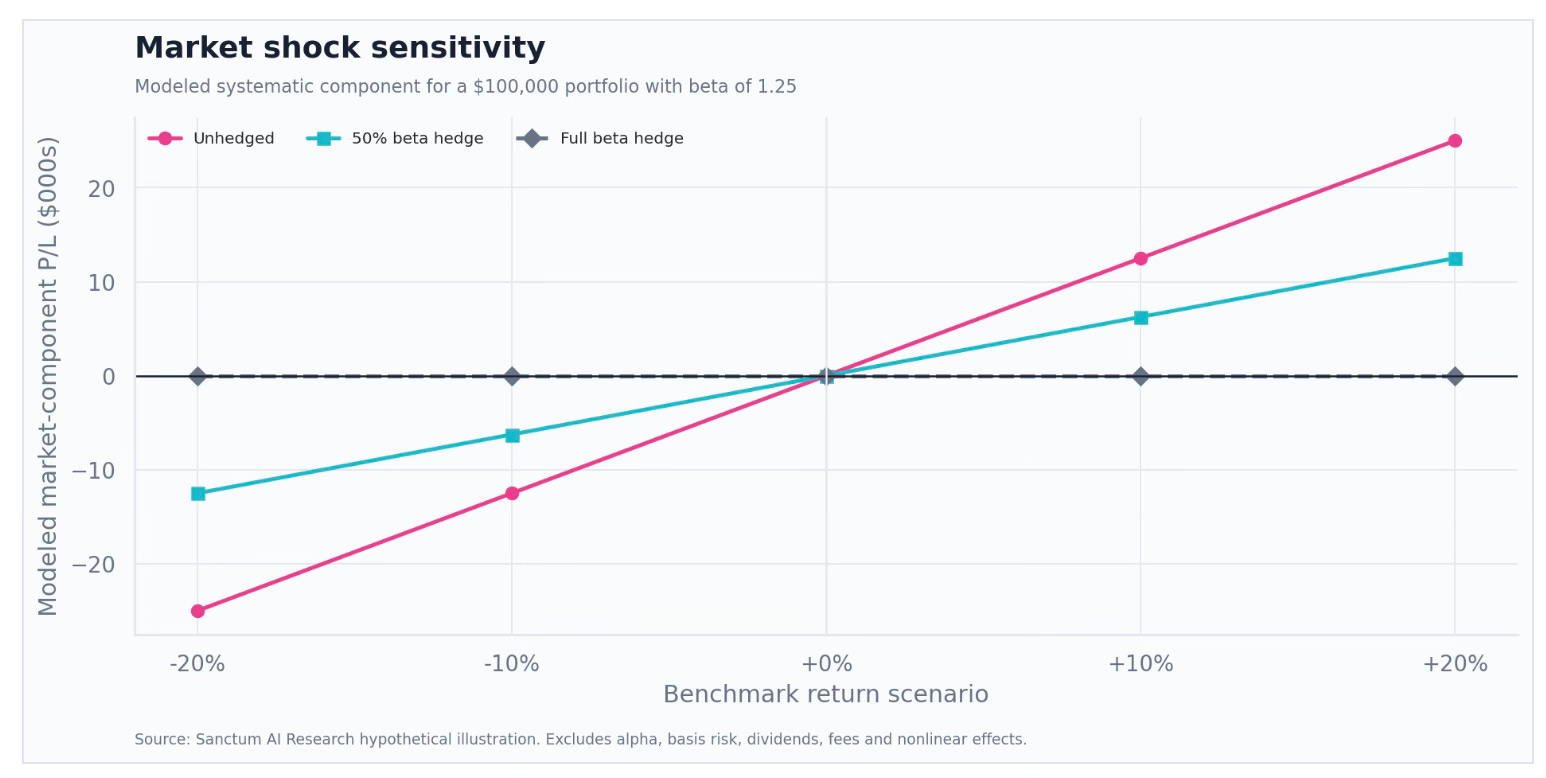

Partial Hedging Usually Beats the Illusion of Perfection

The chart below isolates only the hypothetical portfolio’s modeled market component. It assumes a $100,000 portfolio with beta of 1.25 and ignores alpha, dividends, fees, tracking error, and changes in correlation.

A 50% beta hedge cuts modeled market sensitivity in half. A full beta hedge neutralizes the modeled benchmark component, but not company-specific losses, factor mismatch, gaps, liquidity stress, or estimation error.

This is why a 100% hedge is not the same thing as safety. It is only a 100% hedge against the risk captured by the model.

If the portfolio falls because its companies miss earnings while the benchmark remains flat, an index hedge may offer little help. If correlations jump during a crisis, the hedge may perform better or worse than expected. If the portfolio’s beta changes as holdings move, the original hedge ratio becomes stale.

Most investors are better served by choosing a tolerable residual exposure. A 25% to 50% beta hedge can materially soften broad-market damage while preserving meaningful upside. The correct fraction depends on horizon, conviction, liquidity, taxes, mandate, and willingness to pay.

Choosing the Instrument

1. Reduce Positions or Raise Cash

The cleanest hedge is often less exposure. Selling part of a portfolio has no basis risk, option decay, daily reset, or margin call.

Its costs are equally real: taxes, lost upside, disruption of long-term holdings, and the challenge of deciding when to buy back. Cash is not a sophisticated derivative, but institutions treat liquidity as a strategic risk-management asset.

2. Short an Index ETF

A direct index short creates approximately linear downside protection: when the index falls, the short generally gains; when the index rises, the short loses.

Advantages include transparency, liquidity in major funds, and straightforward sizing. Risks include unlimited theoretical loss, borrow cost, dividends owed by the short seller, margin requirements, and basis risk between the ETF and the portfolio.

3. Equity Index Futures

Futures are a standard institutional hedging instrument because they provide capital-efficient, liquid index exposure. CME Group describes equity index futures as cash-settled contracts used to hedge or express views on an index.

The common sizing formula is:

Contracts = Portfolio value × Portfolio beta × Hedge fraction / Futures contract value

Contract value is the futures price multiplied by the contract multiplier. The result must be rounded to whole contracts, which can make small portfolios difficult to hedge precisely. Futures also introduce leverage, variation margin, expiration, roll management, and overnight gap risk.

4. Protective Puts

A put gives its owner the right, but not the obligation, to sell an underlying asset at a specified strike by a specified expiration. A protective put keeps upside exposure while creating nonlinear downside protection.

That asymmetry is attractive, but it is not free. The premium can expire worthless. The option loses time value, its sensitivity changes with price and volatility, and protection ends at expiration. Buying protection after volatility has surged can be exceptionally expensive.

Cboe identifies protective puts, collars, and index options as common approaches and emphasizes that protection is generally better planned before turbulence raises its price. The SEC also warns that an option buyer can lose the entire premium paid.

Options must be sized by delta, not just contract notional. One option contract usually represents 100 shares, but a put with a delta of -0.30 initially offsets only about 30 shares of underlying exposure, all else equal. Delta changes as the market, time, and implied volatility change. That is why an option hedge must be monitored and periodically rebalanced.

5. Collars and Put Spreads

A collar typically combines a long protective put with a short call. The call premium helps finance the put, reducing the hedge cost in exchange for capping some upside.

A put spread buys one put and sells a lower-strike put. It protects a defined range of losses but stops adding protection below the lower strike.

These structures are useful when an investor can define the exact loss interval that matters. They are dangerous when the investor remembers the premium savings but forgets the payoff they sold.

6. Inverse ETFs

Inverse ETFs are accessible and place the maximum direct loss at the capital invested when purchased without margin. But many inverse and leveraged products target a daily result. Over longer periods, compounding and volatility can cause returns to diverge substantially from the simple inverse of the benchmark.

FINRA warns that most geared products reset daily and may deviate significantly from their stated multiple over longer holding periods, particularly in volatile markets. They are trading and tactical hedging tools, not set-and-forget insurance.

Basis Risk: The Hedge You Bought Is Not the Portfolio You Own

Basis risk is the mismatch between the portfolio and the hedge instrument.

A broad-market hedge against a concentrated growth portfolio may remove general equity beta but leave growth-factor and sector exposure. A semiconductor hedge may offset chip holdings well but poorly hedge software. A small-cap portfolio hedged with a mega-cap index may behave unexpectedly when market leadership rotates.

Institutions evaluate hedge quality using:

correlation and beta stability across multiple windows;

tracking error after the hedge;

sector and factor overlap;

performance in stress periods;

liquidity during disorderly markets;

carry cost and implementation slippage.

High correlation in calm markets is not enough. The hedge must work when it is needed.

The Cost of Protection

Hedges reduce expected return unless they possess a separate positive expected return. The cost may appear in different forms:

option premium and time decay;

upside surrendered through a short position or covered call;

futures financing, roll, and margin costs;

ETF expenses and compounding drift;

short borrow fees and dividends;

bid-ask spreads, commissions, and taxes;

opportunity cost when protection remains active during a rally.

This creates a fundamental rule:

Hedge the risk that can impair the portfolio, not every fluctuation that makes you uncomfortable.

Permanent protection can become a permanent return drag. Tactical protection can fail because timing is difficult. The compromise is a policy that defines acceptable cost and adjusts exposure gradually.

A Practical Hedge Policy for a Hypothetical Investor

An institutional process is written before the market becomes emotional. A simplified policy might look like this:

Define the benchmark. Choose the index that best represents the portfolio’s economic exposure, not the most familiar ticker.

Estimate risk using several windows. Compare shorter and longer beta, correlation, volatility, and factor exposure. Do not trust a single regression.

Set the objective. Decide whether the hedge targets beta, volatility, drawdown, event risk, or a specific loss band.

Choose residual exposure. Instead of asking “How much should I short?” ask “How much market sensitivity do I still want?”

Select the simplest suitable instrument. Position reduction and cash come before complex derivatives. Options are appropriate when nonlinear protection is worth its premium.

Cap implementation risk. Set limits for gross exposure, leverage, premium budget, maturity, liquidity, and counterparty or borrow risk.

Rebalance deliberately. Review when portfolio weights, beta, price, delta, volatility, or regime changes beyond predefined tolerances.

Write the exit rule at entry. Protection without a removal rule often becomes an expensive long-term habit.

A regime-based schedule could increase protection in steps rather than jump from zero to fully hedged:

Normal conditions: no tactical hedge or a small strategic hedge;

Risk building: modest partial hedge;

Confirmed deterioration: larger beta hedge and higher cash;

Mandate-level drawdown: reduce gross long exposure rather than endlessly layering derivatives.

The thresholds should be based on the investor’s own risk capacity and tested process. They should not be improvised from headlines.

The Seven Most Common Hedging Mistakes

Hedging dollar value instead of risk exposure. Portfolio beta and hedge beta are ignored.

Using the wrong benchmark. The hedge looks liquid but does not match the portfolio’s real factor mix.

Buying protection after volatility explodes. The investor pays the highest insurance premium after the accident has started.

Overhedging. The portfolio becomes accidentally net short or sacrifices the alpha thesis.

Ignoring path dependence. Daily-reset inverse products are held as though their objective applies indefinitely.

Failing to rebalance. Portfolio weights, beta, option delta, and contract value change while the hedge remains frozen.

Having no exit rule. A temporary hedge quietly becomes a permanent drag.

The Real Goal

Hedging is not about feeling clever during a selloff. It is about staying solvent, disciplined, and capable of acting when opportunity appears.

The institutional mindset is surprisingly simple:

Measure the risk. Define the loss you cannot accept. Choose the cleanest offset. Size it against exposure. Account for cost. Monitor the mismatch. Remove it by rule.

Done properly, a hedge does not replace a strong portfolio. It gives that portfolio a better chance to survive the environments for which it was not built.

This article is for educational purposes only and does not constitute investment, legal, or tax advice. All portfolio values and scenarios are hypothetical. Beta, covariance, correlation, volatility, option Greeks, and other estimates are unstable and may change materially. Derivatives, short sales, leveraged products, and inverse products involve substantial risk and may not be appropriate for every investor.