META Compute and the Neo-Cloud Reset

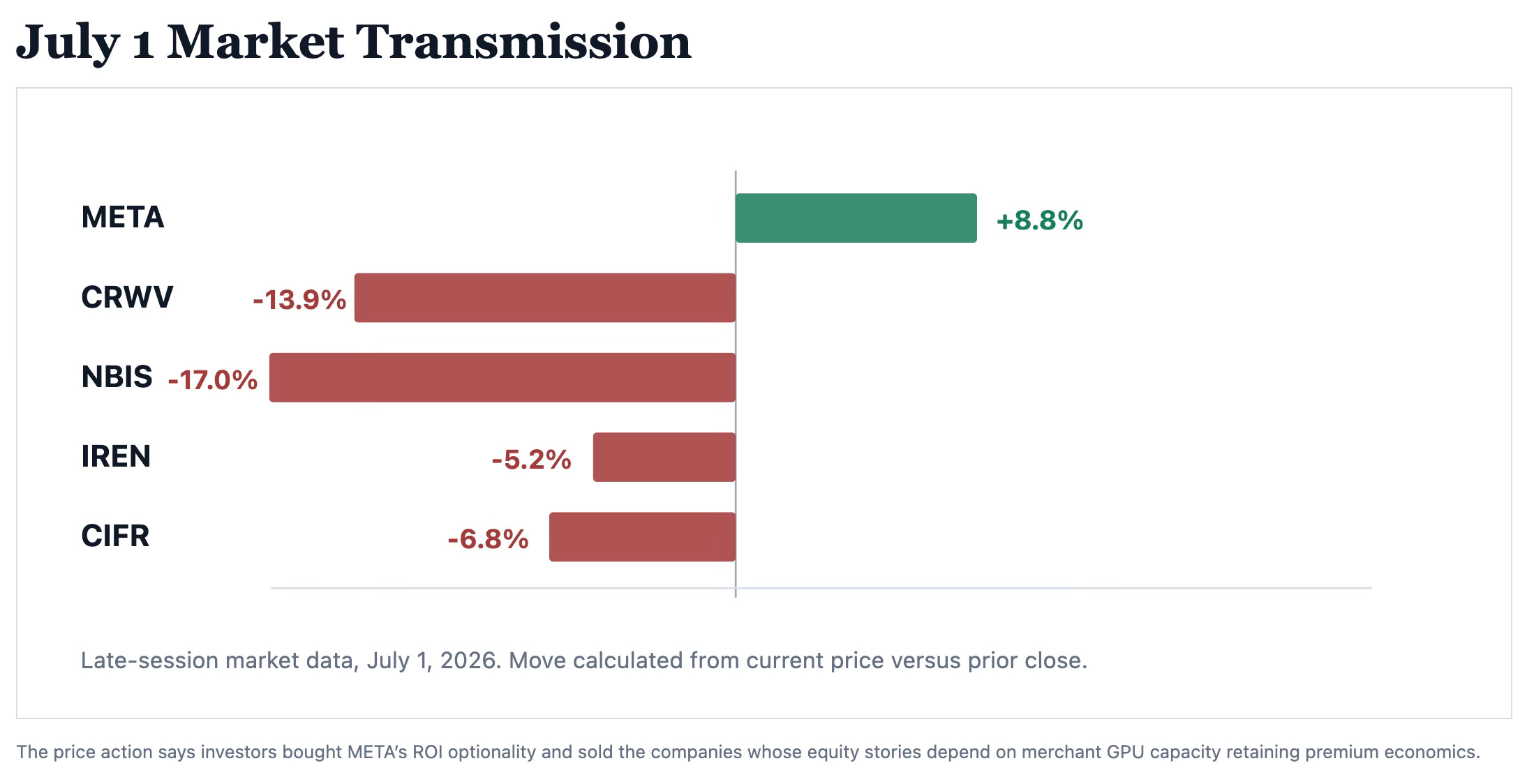

Meta’s reported plan to commercialize excess AI compute is not automatically fatal for CoreWeave, Nebius, or the broader AI infrastructure complex. It is, however, a credible challenge.

SANCTUM VERDICT

Not a nothing burger. Not a death blow.

The real risk is multiple compression before revenue impairment. META does not need to steal today’s backlog to hurt neo-cloud equities. It only needs to convince investors that future GPU capacity is less scarce, more price-discoverable, and more exposed to hyperscaler balance sheets.

Base case: META becomes a new utilization valve and potential price reference, not an overnight replacement for purpose-built AI clouds. The equity impact is highest where valuation assumes scarcity, backlog permanence, and high terminal returns on GPU assets.

What Actually Changed

Fact: Bloomberg reported that Meta is developing a cloud infrastructure business to sell access to AI computing power and models. The reported construct includes external access to hosted models and potentially raw compute capacity.

Fact: Meta already told investors that 2026 capex is expected to land between $125B and $145B, with the increase driven by component pricing and data center costs tied to future capacity.

Judgment: The market is not only reacting to a new competitor. It is reacting to a potential change in the industry’s clearing price for AI compute.

If excess hyperscaler compute becomes merchant supply, the neo-cloud model moves from scarcity premium toward underwriting discipline.

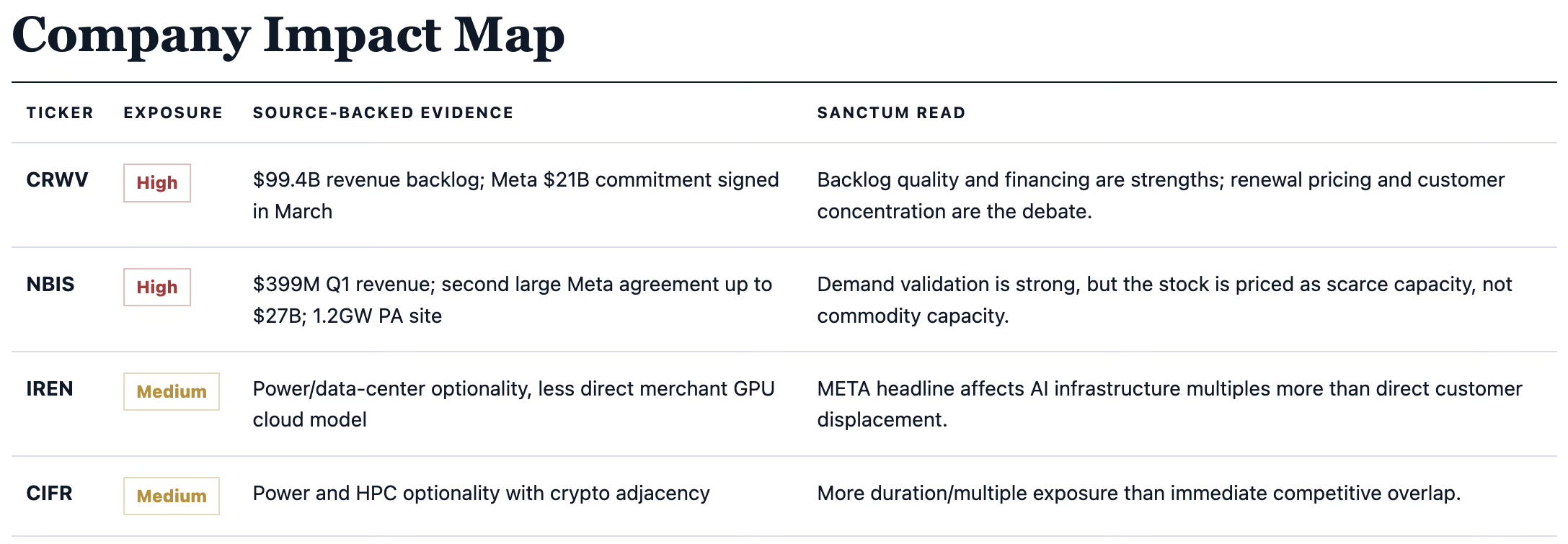

CRWV vs NBIS: The Real Debate

CoreWeave

CoreWeave has the cleaner proof of scaled execution: $99.4B backlog, multi-year hyperscaler/AI-lab demand, more than 1GW active power, and deep financing access. That is not fragile.

The vulnerability is not whether CRWV has demand today. It is whether future contracts renew at the same economics if a hyperscaler with an enormous balance sheet begins offering comparable raw compute capacity.

Nebius

Nebius has powerful demand validation: Q1 revenue acceleration, positive adjusted EBITDA, a large Meta-linked agreement, and a 1.2GW Pennsylvania AI factory plan.

The vulnerability is duration and expectations. When a stock is capitalizing years of capacity growth, a new potential price-setter can compress the multiple even before reported revenue breaks.

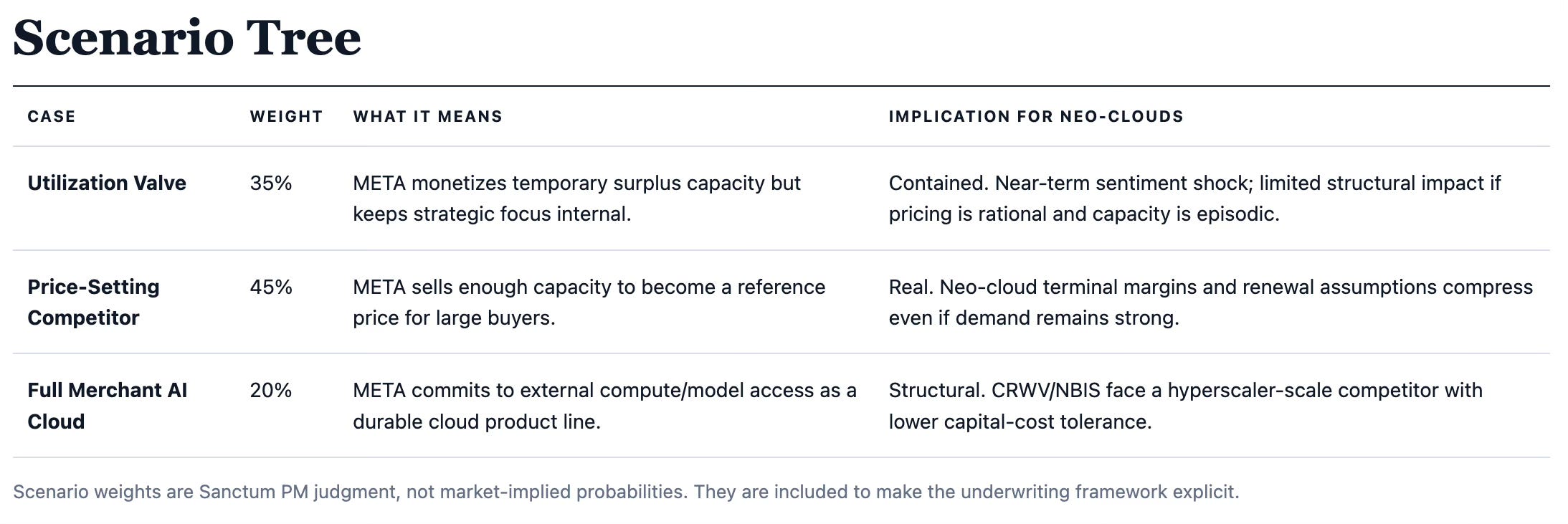

What Would Prove It Is Real

META confirms product: Named SKU, external customer roster, model hosting terms, pricing page, or segment language.

Capacity is not transient: Public commitment that merchant compute is a standing business, not opportunistic overflow.

Neo-cloud pricing moves: Spot/reserved GPU pricing drops, shorter contract tenor, lower prepayment, or less favorable financing.

Backlog starts repricing: CRWV/NBIS renewal language weakens, RPO conversion slows, or customer concentration worsens.

Demand absorbs supply: Utilization stays high, pricing remains firm, and META continues buying from third-party neoclouds.

Investment Conclusion

META: The headline is equity-positive because it creates a return-on-capex narrative around infrastructure that investors were starting to question. It does not need to become AWS to matter; it just needs to monetize underutilized capacity enough to reduce perceived waste.

CRWV / NBIS: The selloff is directionally rational but probably too blunt. Backlog and demand do not disappear because META explores merchant compute. The better framework is to haircut terminal GPU rental margins, stress renewal pricing, and demand higher proof that backlog converts at attractive returns.

Bottom line: This is a valuation architecture event. It changes how the market should underwrite scarcity, not necessarily how many GPU hours get consumed.