MORE INFORMATION ≠ BETTER TRADES

There was a time when the retail trader’s disadvantage was obvious: the pros had the terminals, the research, the speed, the contacts, the flow. Today, that story is harder to tell. A new trader can wake up, open five apps, watch live market TV, read earnings transcripts, scan fifty charts, scrape sentiment, ask an AI tool for a summary, and sit in three group chats before the opening bell. The modern problem is not scarcity. It is abundance. And abundance has its own failure mode. Herbert Simon saw it decades ago: in an information-rich world, what becomes scarce is attention.

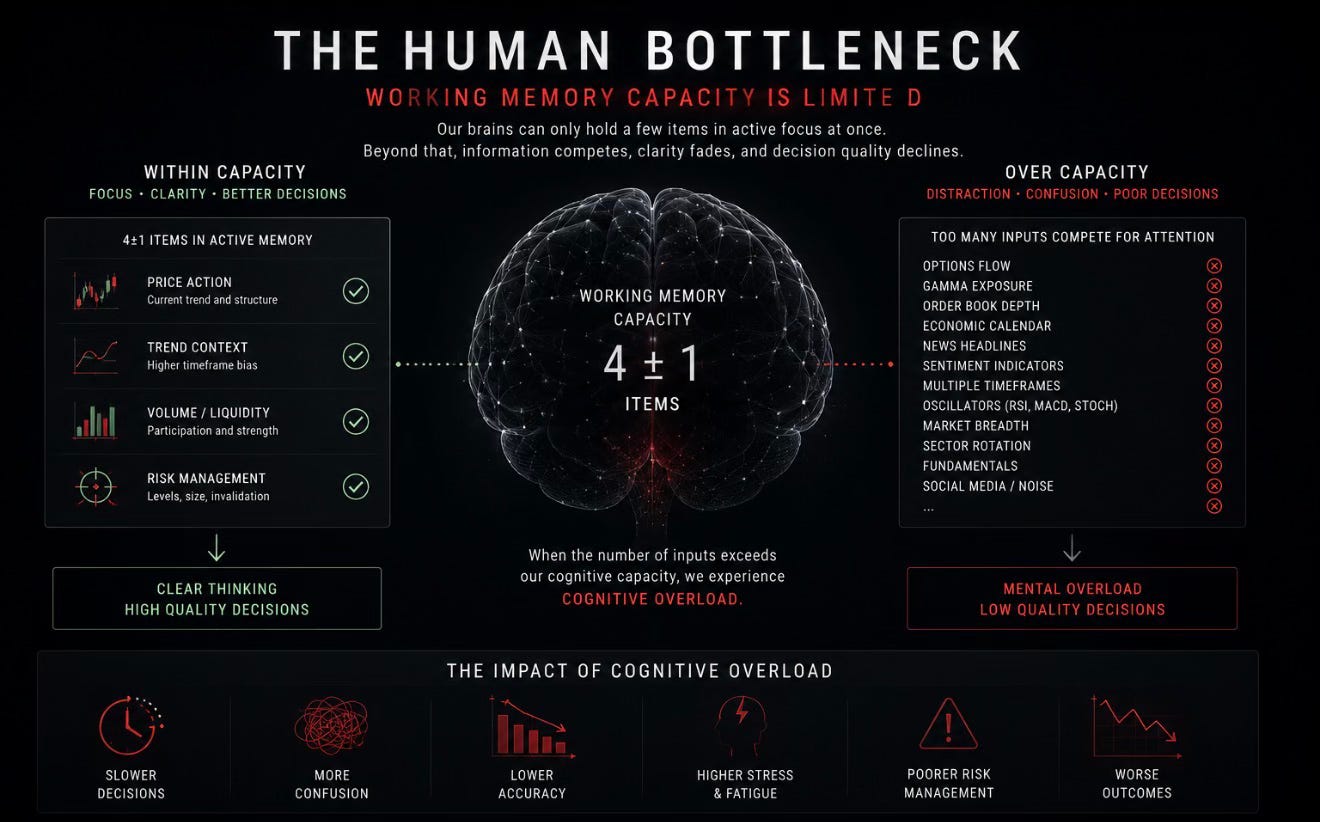

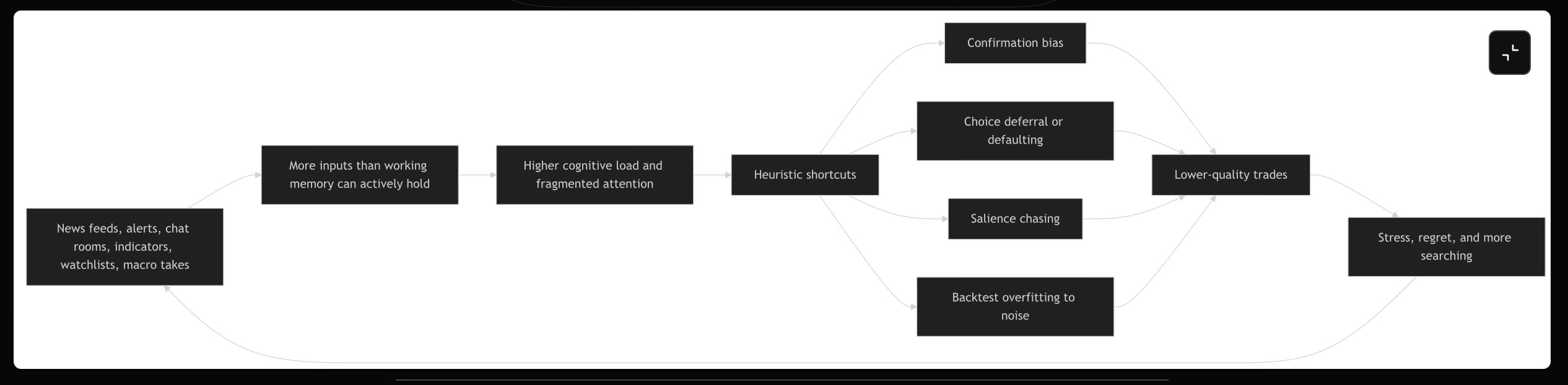

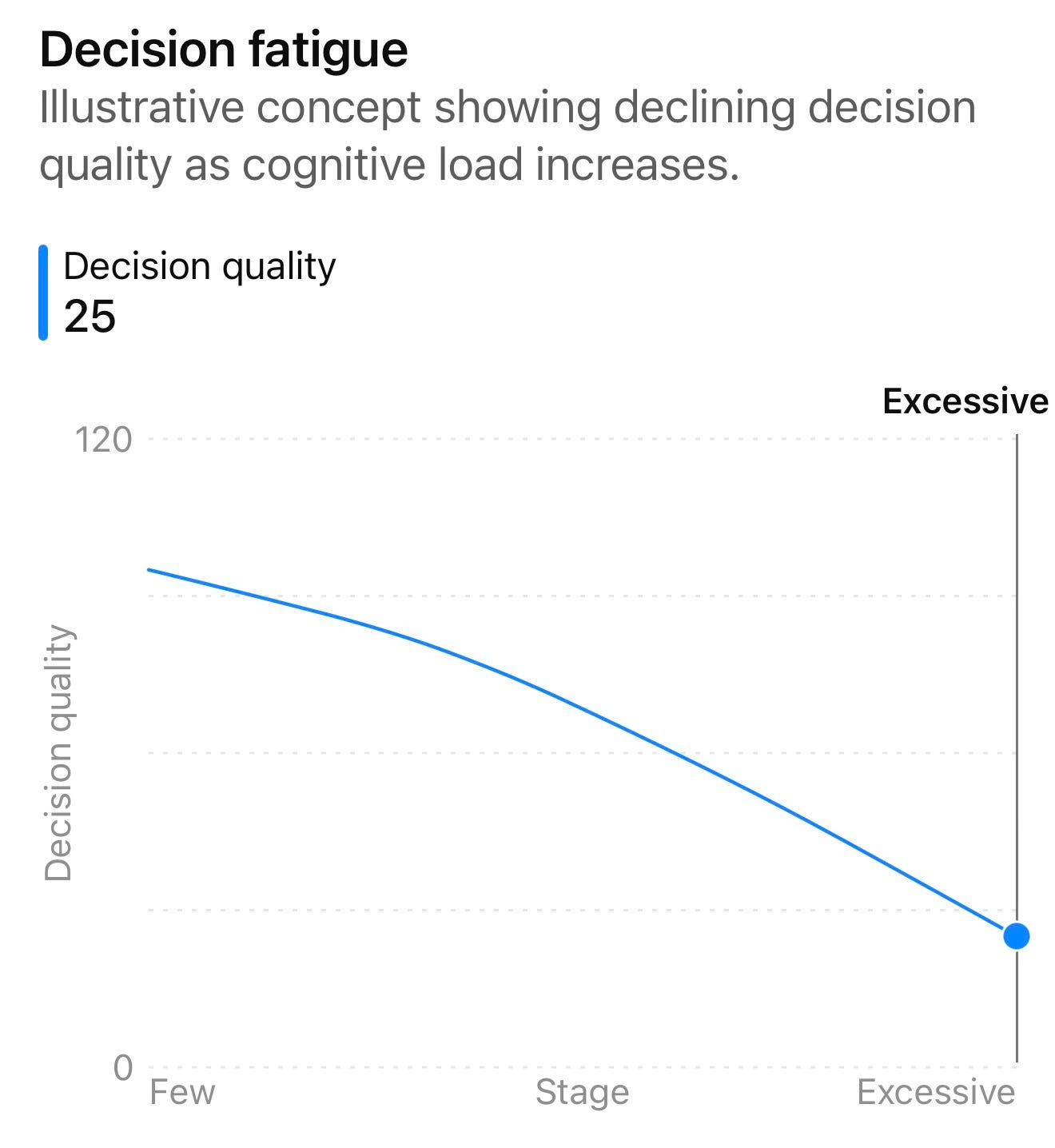

That sounds abstract until you look at how the mind actually handles complexity. Working memory is not a giant hard drive you can keep stuffing with inputs. Nelson Cowan’s review puts the active limit at roughly three to five meaningful items. Cognitive load theory, going back to Sweller, says that when a task gets too cluttered, processing capacity gets burned on managing the clutter itself. For a trader, that means the tenth input is not just “one more thing to consider.” It may crowd out the only thing that mattered.

And here is where it gets dangerous: more information does not necessarily make you humbler. Sometimes it does the opposite. In a set of experiments on prediction, Crystal Hall and her coauthors found that extra information could make people less accurate and moreconfident at the same time. They called it an illusion of knowledge. Anyone who has ever spent two hours building a gorgeous trade thesis around a stock that was really just drifting with the tape already knows the feeling. The story gets richer. The decision does not get better.

Once overload hits, the mind looks for shortcuts. That is not a moral failure. It is what bounded cognition does. Confirmation bias makes us seek evidence that flatters the position we already want to hold. Choice overload makes us defer, default, or chase the easiest-looking option. In markets, that often means one of three things: you freeze and miss the trade, you lunge at the loudest ticker, or you keep “researching” long after the decision has stopped improving. Retail traders usually call this analysis paralysis. The literature calls it choice deferral and biased evidence processing. Same movie, cleaner subtitles.

Finance research shows these are not just armchair observations. Brad Barber and Terrance Odean found that individual investors are net buyers of attention-grabbing stocks. The reason is intuitive. If you cannot search the whole market, you buy what stands out. Salience becomes a sorting mechanism. David Hirshleifer and his coauthors show that when firms announce earnings on crowded news days, the market reacts more sluggishly and drift is stronger afterward. Stefano DellaVigna and Joshua Pollet find something similar for Friday earnings announcements: less immediate response, more delayed adjustment. When too much is happening at once, markets do not become more efficient. They become slower to digest what matters.

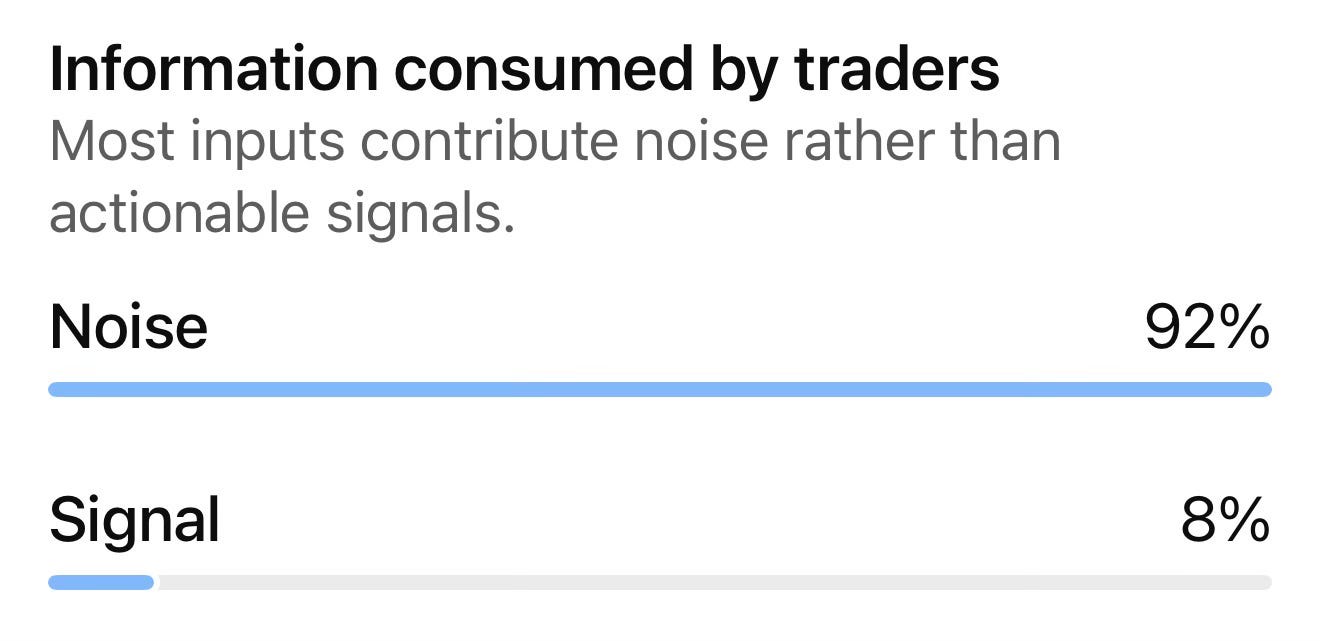

The most direct evidence comes from a Federal Reserve paper I found yesterday that tries to measure information overload itself. Using textual analysis of New York Times coverage back to the nineteenth century, the authors build an information-load index and find something subtle but important. A moderate increase in information may pull attention toward markets. But when information becomes high or excessive, it is followed by lower trading volume and higher future returns. The interpretation is not that information is useless. It is that past a certain threshold, investors stop processing it well. Estimation risk rises. Attention fragments. Prices temporarily underreflect what is in front of everyone.

This matters even more for newer traders because their filters are still weak. In retirement-choice experiments, lower-knowledge participants were dramatically more likely to default than higher-knowledge participants, and simplification helped mainly the more knowledgeable group. In other words, when you have not yet built a mental model for the task, the problem is not just the interface. The task itself is overwhelming. That maps neatly onto the beginner trader who is still trying to decide whether to follow momentum, mean reversion, macro, earnings, options flow, or someone on X with a spaceship emoji avatar.

The app era may make this worse, not better. Brokerage push notifications increase trading activity shortly after they arrive. Attention-trigger studies show that the trades induced by these prompts carry higher leverage on average, and the effects are stronger for younger and less experienced investors. Gamified design increases activity too. None of this proves that every notification is harmful. It does show that “more information” is often delivered as an attention hack rather than as a decision aid.

The irony is that attention itself can be valuable. One brokerage-data study finds that investors who pay attention more effectively can perform better. So the lesson is not to become proudly uninformed. It is to separate signal from stimulation. Traders who survive long enough usually learn the same quiet rule: the goal is not to know more things. It is to know fewer things more clearly.

That also explains why overfitting is such a seductive retail trap. A trader who feels overwhelmed by the mess of the market often reaches for more indicators, more parameter tweaks, more filters, more “confluence.” But in finance, the signal-to-noise ratio is low enough that testing endless variations on the same historical data almost guarantees false positives. You can make the past look incredibly orderly if you try enough versions. The market does not reward that kind of intelligence. It punishes it.

So the real retail edge may be embarrassingly unsexy. Fewer alerts. Fewer watchlist names. One setup at a time. A prewritten checklist. A rule that every thesis must name the one fact that would invalidate it. A hard stop on how many decisions you will make in a day. A separation between research time and execution time. Less “staying informed.” More protecting the bandwidth required to think. The modern trader does not need another firehose. The modern trader needs a valve.

Trader playbook grounded in the research

The practical recommendations that follow are strongest when presented not as self-help advice but as cognitive risk controls.

Build an information hierarchy. The evidence supports a simple filtration principle: a small number of high-value sources beats a sprawling feed. One primary price/volume source, one event calendar, one news source, and one journal or post-trade notebook is usually enough for a retail process. This recommendation follows directly from working-memory limits, choice-overload findings, and the salience-driven behavior documented in retail-investor research.

Cap the size of the opportunity set. A watchlist with 12 names is cognitively different from a watchlist with 120. The 401(k) literature and Agnew/Szykman experiments suggest that too many options raise overload, increase defaults, and reduce participation or quality of choice. For traders, a smaller opportunity set reduces the search problem that otherwise pushes attention toward whatever is loudest.

Separate research from execution. Do your broad reading when the market is closed, not while trying to enter or manage a trade. This follows from cognitive-load theory and finance evidence on distraction: when too many live cues compete, reactions get slower and more error-prone. A written premarket plan can turn open-market decisions from improvisation into recognition.

Use explicit decision rules. Checklists, signal thresholds, position-sizing formulas, and “if/then” rules reduce moment-to-moment processing demand. That is exactly the kind of schema support Sweller’s framework implies novices need. It is also a defense against analyst-style fatigue effects, where later decisions become more heuristic.

Adopt a disconfirming-evidence ritual. Before entering any trade, require one paragraph -or one line in your journal- answering: What would prove me wrong? This is the cleanest practical response to confirmation bias. It forces an active search for non-flattering evidence rather than passive collection of supportive noise.

Treat notifications as optional, not neutral. The literature on push notifications, attention triggers, and gamification suggests these features change trading behavior, risk-taking, and activity even when the underlying information is public and ordinary. Turning most alerts off is not laziness. It is a refusal to let the interface set your agenda.

Run an information diet. One practical template: no financial social media during market hours except for a preselected event list; no more than one post-close review source; no reactive content after placing a trade unless it changes a predefined risk or thesis condition. This recommendation is an inference from the overload/distraction literature rather than a directly tested “diet” protocol, but it is well aligned with the mechanisms identified in the cited work.

Assume every extra backtest degree of freedom is a liability. Every added indicator, lookback tweak, stop variant, or exit rule raises the chance that you are fitting noise. Keep a log of how many variants you tried, hold out a truly untouched sample where possible, and prefer simple models that survive across regimes over baroque models that dominate a single in-sample period.

Limit decision count, not just screen time. The analyst-fatigue evidence suggests that repeated decisions can degrade later judgment quality. A practical retail adaptation is to cap the number of discretionary trades or setup evaluations per day. After that cap, you review; but you do not act.

Judge your process by ex ante clarity, not post hoc storytelling. Oskamp’s classic study and Hall’s later experiments both warn that more information can inflate confidence without improving accuracy. That means traders should beware of post-trade narratives that sound sophisticated but were not part of the original edge. The cleaner metric is: Was the setup defined in advance, and did I follow it?