Stock Dilution: The Fine Print That Can Kill a Chart

All you need to know about dilution.

You wake up, check the ticker, and the stock is down 18% premarket. The press release says something like:

“Company announces $75 million registered direct offering priced at-the-market.”

Or worse:

“Company enters into securities purchase agreement with institutional investors.”

Or the nuclear version:

“Company files resale registration statement related to convertible notes and warrants.”

To newer traders, this all sounds like corporate legal language. To people who have been around small caps long enough, it sounds like a trapdoor opening under the stock.

Dilution is one of the most important things every trader and investor needs to understand. Not because every offering is bad. Not because every company that raises money is a scam. Companies need capital. Growth requires money. Biotechs need to fund trials. Hardware companies need inventory. Miners need equipment. Energy companies need infrastructure. Startups need runway.

But the market does not care about good intentions.

The market cares about supply and demand.

When a company issues more shares, more warrants, more convertibles, or more equity-linked securities, it can increase the amount of stock that may eventually be sold into the market. If demand does not increase enough to absorb that new supply, the price usually pays the bill.

That is dilution in its simplest form.

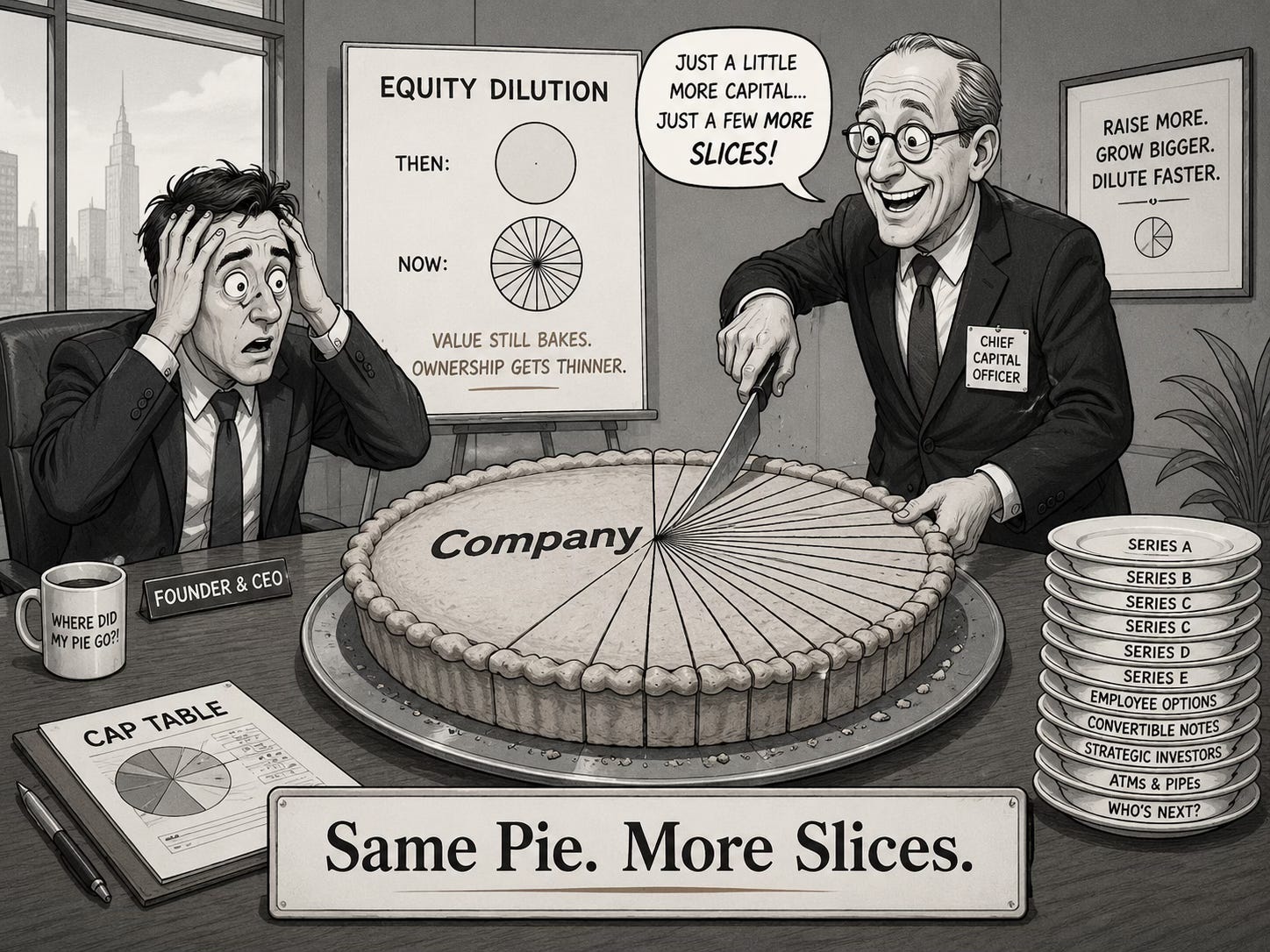

More shares chasing the same business.

Same pie. More slices.

The problem is that not all dilution is created equal. Some dilution is clean, strategic, and even bullish over time. Other dilution is toxic, predatory, and designed in a way that almost guarantees pressure on the stock.

This guide is meant to be something you can come back to every time you see an offering headline and ask:

Is this normal capital raising? Or is this the machine turning on? How screwed am I?

What Dilution Really Means

Dilution happens when a company increases the number of shares or potential shares outstanding.

If a company has 10 million shares outstanding and you own 1 million shares, you own 10% of the company. If that company issues another 10 million shares and you still own 1 million, your ownership drops to 5%.

Nothing happened to your share count.

But your ownership got diluted.

In public markets, dilution also affects the stock because new shares often become future selling pressure. If the company sells stock to investors, those investors may hold, hedge, flip, short against warrants, or sell into liquidity. If the company issues convertible notes, the lender may eventually convert debt into equity and sell shares. If the company has an ATM facility, it may quietly sell shares into the open market over time.

It changes the float. It changes ownership. It changes supply. It changes incentives, and most importantly for you, it f*cks the chart.

Why Companies Dilute

Before we get into the ugly stuff, it is important to say this clearly:

Dilution is not automatically evil.

A company with no cash has limited options. It can raise equity, issue debt, sell assets, cut costs, find a strategic partner, or die. Sometimes raising money is the responsible move.

A biotech with a promising drug may need to raise capital to fund Phase 2 or Phase 3 trials. A semiconductor company may need cash to scale production. A clean energy company may need capital to fulfill a major contract. A company with a stretched balance sheet may raise equity to pay down debt and avoid bankruptcy.

In those cases, dilution can be painful in the short term but necessary for survival or growth.

The real question is not simply:

“Did they dilute?”

The better question is:

“What did they dilute for, at what price, under what terms, and who benefits?”

That is where the truth usually shows up.

A company raising money from a respected strategic investor at a premium to market is very different from a company issuing convertible notes to a lender that can convert at a discount to the lowest trading price.

One is capital formation and the other can be a death spiral.

The Cleanest Form: Traditional Equity Offering

The most straightforward dilution is a common stock offering. The company sells new shares to investors, usually through an underwriter or placement agent. The press release will say how many shares were sold, at what price, and how much money the company raised.

Example:

A company has 20 million shares outstanding. It announces a 5 million share offering at $4 per share. The company raises $20 million before fees. After the offering, the share count rises to 25 million.

That is dilution.

The existing shareholders now own a smaller percentage of the company. But this type of offering is not always bad. It depends on context.

If the stock has run from $2 to $8, the company has no debt, demand is strong, and it raises money at $7.50 to expand production, the market may digest it. It may even be healthy. The company used strength to raise capital and extended its runway.

If the stock is already bleeding, cash is almost gone, and the offering prices 35% below the last close, that is different. That tells you the company was desperate or investors demanded a major discount.

The key things to check are:

Was the offering priced close to market or deeply discounted?

How much dilution is created relative to the existing share count?

Is the cash going toward growth, survival, debt repayment, or vague “general corporate purposes”?

Are there warrants attached?

Is there a lock-up?

Who bought the deal?

A clean common stock offering is usually the easiest form of dilution to understand. The damage is visible upfront. You can calculate the new share count. You can estimate the cash raised. You can decide whether the new balance sheet justifies the new supply.

The more complicated the structure gets, the more careful you need to be.

The ATM: The Silent Seller

An ATM, or at-the-market offering, allows a company to sell shares directly into the open market over time.

This is one of the most misunderstood forms of dilution.

An ATM is not usually a one-day offering. It is a facility. The company registers the right to sell up to a certain dollar amount of stock whenever it chooses, usually through a sales agent.

Example:

A company files a $100 million ATM program. That does not mean it sold $100 million of stock that day. It means it now has the ability to sell up to $100 million into the market over time.

This can be relatively harmless for large liquid companies. For small caps, it can become a constant ceiling over the stock.

Why?

Because every rally can become liquidity for the company to sell into (cough cough MSTR 0.00%↑ ) .

You see the stock spike on news. Volume floods in. Traders think a breakout is coming. Meanwhile, the company may be using that volume to issue shares through the ATM ( cough cough IREN 0.00%↑ ) .

The chart starts acting strange. Every push gets faded. Every breakout loses steam. Buyers show up, but the stock cannot move.

That is often what an active ATM feels like.

The frustrating part is that investors may not know exactly when shares are being sold until the company reports it later in filings. This makes the ATM a quiet dilution machine. It is not always toxic, but it can suppress momentum if the company leans on it aggressively.

When you see an ATM headline, look for the size of the facility relative to market cap and average daily volume.

A $50 million ATM for a $5 billion company is not a big deal.

A $50 million ATM for a $120 million company is very different.

That is potentially a lot of supply waiting above the market.

Registered Direct Offering: The “We Found Buyers, But It Cost Us” Deal

A registered direct offering is when a company sells securities directly to investors using an already effective registration statement.

These deals are common in small caps. They can include common stock, pre-funded warrants, regular warrants, or some combination of all three.

The tone of the press release usually sounds clean:

“Company enters into definitive agreements with institutional investors for the purchase and sale of common stock in a registered direct offering.”

The problem is in the terms.

Registered directs often price below the market. They may include warrants. They may be placed with funds that specialize in financing small public companies. Sometimes those investors are long-term capital providers. Sometimes they are there for the structure.

The warrant coverage matters a lot.

If a company sells shares at $2 and includes one warrant for every share purchased with an exercise price of $2.25, the investor is not just buying stock. They are getting upside optionality. That can create a very different incentive structure.

The investor may sell or hedge the common shares and keep the warrants as a free or low-cost upside ticket. If the stock runs later, warrants can become additional dilution.

This is why a registered direct may look like one deal, but actually create two waves of supply:

The shares issued now.

The warrants that may become shares later.

The press release headline rarely tells the whole story. You have to read the securities purchase agreement, warrant terms, and prospectus supplement.

Warrants: The Shadow Supply

Warrants are one of the most important dilution tools to understand.

A warrant gives the holder the right to buy shares at a specific price, called the exercise price, for a certain period of time.

Example:

A company issues warrants exercisable at $5. If the stock later trades at $8, the warrant holder can exercise at $5 and receive shares worth $8. The company gets $5 per share in cash, but new shares are created.

Warrants are not automatically bad. In fact, if exercised for cash, they can bring money into the company.

But from a trading perspective, warrants can act like overhead supply.

If a company has millions of warrants sitting at $3, $4, and $5, those levels may matter. As price approaches them, holders may exercise, hedge, sell stock, or otherwise create pressure.

The worst warrants are not simple fixed-price warrants.

The dangerous ones have features like:

cashless exercise provisions, reset provisions, anti-dilution adjustments, variable pricing, or very low exercise prices.

Cashless exercise means the holder can receive shares without paying the full cash exercise price, usually based on a formula. This may be useful when shares are not freely tradable or when the company does not have an effective registration statement, but it can also create dilution without bringing in meaningful cash.

Reset provisions are worse. They can lower the exercise price if the company later issues stock at a lower price. This protects the warrant holder but punishes common shareholders.

If you are looking at a small cap, always check the outstanding warrants.

A chart can look clean until you realize there is a wall of warrants waiting above the current price.

Pre-Funded Warrants: Shares Wearing a Mustache

Pre-funded warrants are common in offerings. They sound complicated, but the basic idea is simple.

A pre-funded warrant is almost like common stock. The investor pays nearly the full share price upfront and has the right to exercise into common shares later for a tiny remaining amount, often $0.001 per share.

Companies use pre-funded warrants for investors who do not want to cross certain ownership thresholds, such as 4.99% or 9.99%. From a dilution perspective, you should usually treat pre-funded warrants as basically shares.

They may not be counted as common shares outstanding yet, but they are very close to becoming common shares. This matters because some traders look only at basic shares outstanding and miss the fully diluted picture. If a company has 20 million shares outstanding and 15 million pre-funded warrants, the real potential share count is much higher than the headline number suggests.

Always think in terms of fully diluted shares.

Not just current shares.

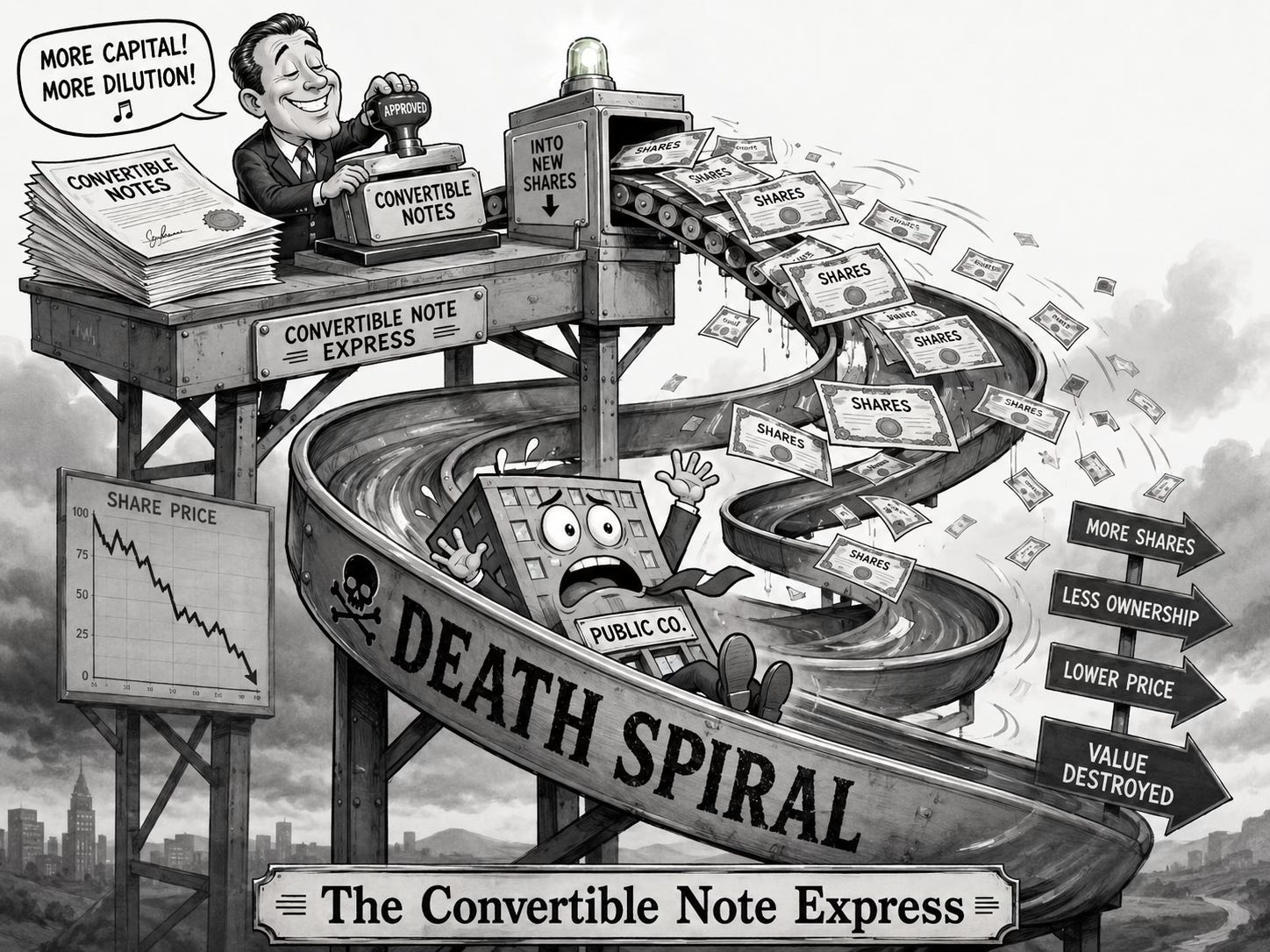

Convertible Notes: Debt That Can Become Stock

Convertible notes are debt instruments that can convert into equity.

There are clean convertibles and toxic convertibles.

A clean convertible might be issued by a strong company at a fixed conversion price. For example, a company borrows money and the lender has the right to convert into stock at $20 per share. If the stock never goes above $20, the note may simply behave like debt. If the stock rises far above $20, the note converts and creates dilution, but at a price that likely reflects business success.

That is not the scary version.

The scary version is variable-rate convertible debt.

This is where things get ugly.

Some convertibles allow the lender to convert debt into stock at a discount to the market price, sometimes based on the lowest trading prices over a lookback period.

Example:

A note can convert at 85% of the lowest VWAP over the last 10 trading days.

Think about that incentive.

If the stock falls, the conversion price falls. If the conversion price falls, the lender receives more shares for the same amount of debt. If the lender receives more shares, they can sell more shares. If they sell more shares, the stock can fall further.

That is the death spiral.

The lower the stock goes, the more shares are needed to repay the debt.

This can absolutely destroy common shareholders.

Variable-rate convertibles are among the most toxic forms of dilution in the market. They are especially common in distressed microcaps that cannot access normal financing.

When you see phrases like “convertible note,” “conversion price equal to a percentage of VWAP,” “alternate conversion price,” “floor price,” “most favored nation,” or “reset,” slow down.

The Death Spiral

A death spiral happens when financing terms create an incentive or mechanism for continuous selling pressure.

The pattern usually looks like this:

A struggling company needs cash.

It issues convertible debt with a variable conversion price.

The lender can convert debt into shares at a discount to market.

The lender sells shares into the market.

The selling pushes the stock lower.

The lower price allows the lender to convert into even more shares.

More shares get sold.

The stock falls again.

Existing shareholders are diluted into oblivion.

Sometimes the company will reverse split to regain compliance or reset the share price. Then the same cycle begins again. This is why some charts look like cliffs.

A stock goes from $10 to $1, reverse splits, then goes from $10 to $1 again. The chart looks “cheap,” but it is not cheap. It is being mechanically diluted. The market cap may keep shrinking while the share count keeps exploding. This is the darkest side of small-cap equity financing. And once you know what to look for, you start seeing it everywhere.

Equity Lines of Credit: “We Can Sell Shares Whenever”

An equity line of credit gives a company the ability to sell shares to an investor over time, often at a discount to market.

It is similar in spirit to an ATM, but the structure is different. Instead of selling into the market through an agent, the company sells shares to a financing partner under a purchase agreement.

These are often marketed as flexible capital. And they can be. But in weak small caps, they can become another steady source of supply. The company draws on the facility. The financing partner receives shares, often at a discount. The financing partner sells those shares. The company gets cash, but the market absorbs more stock.

Again, the key issue is size.

A $25 million equity line for a company with a $500 million market cap may not be dramatic.

A $25 million equity line for a company with a $30 million market cap can be devastating if fully used.

Watch for phrases like:

“common stock purchase agreement”

“equity line”

“committed equity facility”

“purchase notice”

“resale registration statement”

The resale registration is especially important because it often registers shares for resale by the financing partner. That does not always mean they are selling immediately, but it tells you supply may be coming.

Shelf Registration: The Loaded Shelf

A shelf registration allows a company to register securities that it may sell in the future.

The company may register common stock, preferred stock, debt securities, warrants, units, or a mix of securities.

A shelf is not immediate dilution by itself. It is permission to dilute later. Think of it like loading the shelf with inventory. The company is saying:

“We may sell securities when conditions allow.”

Large companies use shelves all the time. It is normal corporate finance. But for small caps, a shelf can matter because it gives the company the ability to move quickly with offerings, especially when the stock spikes. If a stock has a history of raising into every rally, and a fresh shelf becomes effective, traders should pay attention.

Resale Registration: Who Is About to Get Liquidity?

A resale registration statement is different from a primary offering. In a primary offering, the company sells new securities and receives cash. In a resale registration, the company registers shares so existing holders can resell them into the market. This often happens after private placements, convertible financings, warrant exercises, or equity line agreements.

The company may not receive any money when those registered shares are sold. The selling shareholder does.

This is critical.

A headline might say the company filed a registration statement for millions of shares. Traders panic and assume the company is raising money. Sometimes it is not a capital raise. It is registration of shares for resale by prior investors.

But it can still be very bearish if those shares represent a large percentage of the float.

The question is:

Who owns these shares, and are they likely to sell?

If the shares belong to long-term insiders or strategic partners, maybe less concerning.

If the shares belong to financing funds from a discounted private placement, much more concerning.

A resale registration can turn restricted paper into marketable supply.

That can change the entire float dynamic.

Preferred Stock: The Sneaky Senior Security

Preferred stock sits above common stock in the capital structure. It can have dividends, conversion rights, voting rights, liquidation preferences, and special protections.

Some preferred stock is harmless.

Some is brutal.

The danger comes when preferred shares are convertible into common stock using terms that adjust based on price, protect the preferred holder from downside, or give them control over future financing.

Toxic preferred can behave like toxic convertible debt. It may convert at a discount. It may have reset provisions. It may accumulate dividends payable in stock. It may include anti-dilution protections that punish common shareholders if the company raises capital later at lower prices.

This is why you cannot only look for the word “offering.”

Sometimes the dilution is hiding in preferred stock terms. Read the certificate of designation. That is where the bodies are buried.

How to Read an Offering Headline

When an offering headline drops, do not just react to the word “offering.”

Read the structure.

Here is the mental checklist.

First, what type of offering is it?

Common stock, registered direct, private placement, ATM, convertible note, warrant exercise, equity line, or resale registration?

Second, how much money is being raised?

Compare the amount raised to the company’s market cap and cash balance. A $10 million raise for a $2 billion company is small. A $10 million raise for a $20 million company is huge.

Third, what is the price?

If the offering is priced close to the market, that is better. If it is priced at a deep discount, that is a warning.

Fourth, are warrants attached?

If yes, how many? What exercise price? What expiration? Are there reset provisions? Are they cashless? Are they immediately exercisable?

Fifth, is the company receiving cash?

In a primary offering, yes. In a resale registration, usually no. In a warrant exercise, maybe. In cashless exercise, maybe not much.

Sixth, what is the use of proceeds?

Growth, acquisitions, inventory, debt repayment, working capital, or vague corporate purposes?

Seventh, what does the company’s history look like?

Has it diluted repeatedly? Has it reverse split? Does every rally get met with financing?

The headline is only the first clue. The terms are the story. Don’t be Lazy and read the filing.

How to Find the Filings

The best place to find dilution is the SEC’s EDGAR database.

Search the company ticker or name. Then look for filings like:

S-1, S-3, 424B, 424B5, 8-K, 10-Q, 10-K, DEF 14A, SC 13G, SC 13D, and forms related to warrants or convertible securities.

The most important ones for dilution are often:

S-1: Registration statement, often used for resale shares, IPOs, or smaller company offerings.

S-3: Shelf registration for companies eligible to use it.

424B5: Prospectus supplement, often where offering details are laid out.

8-K: Current report, often filed when a company announces a financing agreement.

10-Q / 10-K: Quarterly and annual reports. These usually include share count, warrants, debt, convertibles, liquidity, and going concern language.

DEF 14A: Proxy statement. This can show requests to increase authorized shares or approve reverse splits.

When doing DD, search inside filings for words like:

“warrant”

“convertible”

“conversion price”

“exercise price”

“cashless”

“anti-dilution”

“reset”

“floor price”

“beneficial ownership limitation”

“at-the-market”

“equity line”

“purchase agreement”

“resale”

“going concern”

“authorized shares”

These keywords will quickly tell you whether the company has a clean capital structure or a swamp.

The Most Toxic Dilution Structures

In my view, the most toxic forms of dilution usually share one trait:

They reward the financier while common shareholders take the pain.

The worst structures are usually:

variable-rate convertible notes, floorless convertibles, warrants with reset provisions, equity lines used aggressively by distressed companies, large resale registrations tied to discounted financings, and repeated ATM selling into every rally.

The most dangerous phrase is anything that ties conversion price to a discount of recent market prices. That turns weakness into more dilution. Fixed-price dilution is at least understandable. You can calculate the damage.

Variable-price dilution is harder because the lower the stock goes, the worse the dilution gets.

That is why toxic convertibles are so destructive. They do not just dilute the company once. They can create an ongoing mechanical selling cycle.

When Dilution Can Actually Be Bullish

Now for the nuance.

Not every raise is bearish.

Sometimes an offering is the moment a company removes survival risk.

A biotech with six months of cash raises enough to fund trials for two years. A company with expensive debt raises equity to clean up the balance sheet. A hardware company raises money to fulfill demand from a major customer. A strategic investor buys shares at a premium and brings commercial value.

In those cases, dilution may be short-term pain for long-term upside.

The market may even reward it after the initial shock if investors believe the cash improves the company’s odds of success.

The best dilution is usually:

priced near market or at a premium, done from a position of strength, led by high-quality investors, used for specific growth initiatives, free of toxic warrants or variable convertibles, and large enough to solve a real problem without destroying the cap table.

A company raising money because demand is exploding is different from a company raising money because payroll is due.

Context is everything.

How Dilution Shows Up on the Chart

Dilution has a footprint.

A stock with active dilution often trades heavy. Good news spikes fade. Breakouts fail. Volume appears, but price barely moves. Every rally feels like someone is selling into it. You may see huge volume with no follow-through. That can mean supply is being absorbed, or it can mean new shares are being dumped into demand.

The difference is what happens after.

If the stock absorbs supply and starts making higher lows, buyers may be winning.

If every push gets rejected and the company keeps filing more financing documents, the supply machine may still be active.

Dilution-heavy charts often have the same personality:

sharp pumps, violent fades, endless lower highs, reverse splits, sudden offering headlines, and retail confusion about why “good news” never holds.

This is why dilution DD matters before trading small/mid caps.

A great catalyst can still fail if the company is using the rally as an exit ramp for new supply.

The Float Is Not the Whole Story

Traders love low floats.

Low float stocks can move violently because there are fewer shares available to trade. But the float can be misleading if there is hidden supply waiting to become free trading.

A company may advertise a tiny float while having:

millions of warrants, convertible notes, pre-funded warrants, resale shares, preferred stock, equity line capacity, or an active ATM.

That means the float today may not be the float tomorrow.

This is where many traders get trapped.

They see a low float and assume scarcity. Then an S-1 becomes effective, warrants get exercised, convertibles convert, or the ATM starts selling. Suddenly the float expands and the trade changes.

Always ask:

What is the current float?

What is the fully diluted share count?

What securities can become common stock?

Are those shares registered?

Are holders likely to sell?

Float is not static. In dilution-heavy names, float is a moving target.

Final Thoughts

Dilution is not just a headline. It is a process. It can be clean or toxic. Strategic or desperate. Temporary or endless. It can save a company, or it can slowly bleed common shareholders until nothing is left. The mistake most traders make is treating all offerings the same.

They see “offering” and panic.

Or they see “cash raised” and assume it is bullish.

The real work is in the terms.

What kind of security was issued? At what price? To whom? With what warrants? With what conversion rights? How large is it relative to the company? Is the company raising from strength or weakness? Does the financing solve the problem, or just buy another quarter?

That is how you separate normal dilution from toxic dilution.

The market is full of companies that survive by selling stock, not by building value. Once you understand dilution, you start seeing the game more clearly.

You understand why some rallies fail.

You understand why some “cheap” stocks keep getting cheaper.

You understand why reverse splits are often followed by more pain.

You understand why the filing matters more than the press release.

Most importantly, you stop being the liquidity.