The Art of the Small Caps

The Rigging Games

“They must be manipulating small-cap stocks to set up dilution and offerings, right? Otherwise, what would be the purpose?”

At first glance, that assumption makes sense. When a low-quality small-cap stock suddenly has its float aggressively bought up and squeezed, it is natural to assume there must be a bigger agenda behind it. One common theory is that the move is connected to the company itself, with institutions or market participants helping create a price spike so the company can raise capital through an offering.

But that explanation does not hold up well when tested against reality.

First, many small-cap stocks that appear heavily manipulated or aggressively squeezed do not conduct an offering shortly afterward. In many cases, the stock runs hard, shows signs of coordinated price action, and then no dilution event follows within the next month.

Second, the motive is not always tied to an offering. Sometimes larger players may anticipate that certain upcoming news, earnings, conference calls, partnerships, or announcements involving larger companies will attract major retail attention. In those cases, they may accumulate or push the stock ahead of the event, then sell into the retail demand once attention arrives. In today’s market, squeeze setups are not only built around dilution. There are many different catalysts and narratives that can be used to create momentum.

The bigger point is this: market participants can often make far more money from liquidity extraction than from any side arrangement connected to a company offering.

This is the main reason the “it must be for dilution” explanation is too limited.

The game is often less about arranging a financing deal and more about taking advantage of liquidity. Think of it like collecting chips from the poker table. By forcing a stock higher, attracting chasing longs, unloading inventory into that demand, and then potentially hedging or positioning short while the stock collapses, sophisticated players can generate large profits from the price movement itself (cough cough CAR 0.00%↑ ) . Whether there is an offering, news, or any obvious fundamental reason may not matter.

That is why you sometimes see a ticker squeeze even when it appears to have no obvious offering potential, no major news, limited borrow availability, and no clear fundamental reason to move. The reason may simply be liquidity hunting and P/L extraction.

There is also a practical counterargument to the idea that every manipulated move is tied to dilution. If every major small-cap squeeze were followed by an offering, the pattern would become too obvious. Regulators could more easily investigate the order flow, identify relationships, and look for connections between market participants and corporate financing activity.

For that reason, the randomness may be partly intentional. Some squeezed stocks later receive offerings, while many others do not. This mix creates noise in the data. It makes the pattern harder to detect and harder to trade with consistency.

This also affects traders on both sides. Long traders can still get trapped in names that eventually dilute, while short sellers can also get trapped when they expect an offering that never comes. If offerings followed manipulated moves too reliably, the edge would become obvious. So the outcomes remain mixed: some stocks squeeze and dilute, some squeeze without dilution, and some move for entirely different reasons.

In my own research, when I identified stocks that showed signs of manipulated price action, I tracked those samples over time to see whether offerings consistently followed. The answer was no. Manipulated price action did not reliably predict near-term dilution. If it did, it would be an easy trading edge, and the market rarely leaves edges that obvious untouched.

So the better explanation is that dilution is only one possible motive. The broader and often more important motive is liquidity raiding.

Liquidity raiding refers to the process of forcing traders into bad positions and extracting value from their liquidations, stop-outs, panic covers, and emotional decision-making. In simple terms, it is the institutional collection of open P/L from traders across the market.

The goal is to create price movements that trap leveraged or oversized traders in the wrong places. Once traders are caught offside, their forced exits become liquidity for the larger player. Highly leveraged traders are especially vulnerable because when a position moves against them, emotion, margin pressure, and poor decision-making can take over quickly.

In many cases, the trader does not even need to be highly leveraged. A lack of edge, poor timing, or excessive size can be enough to make them vulnerable to these liquidity raids.

Let’s use a simple example.

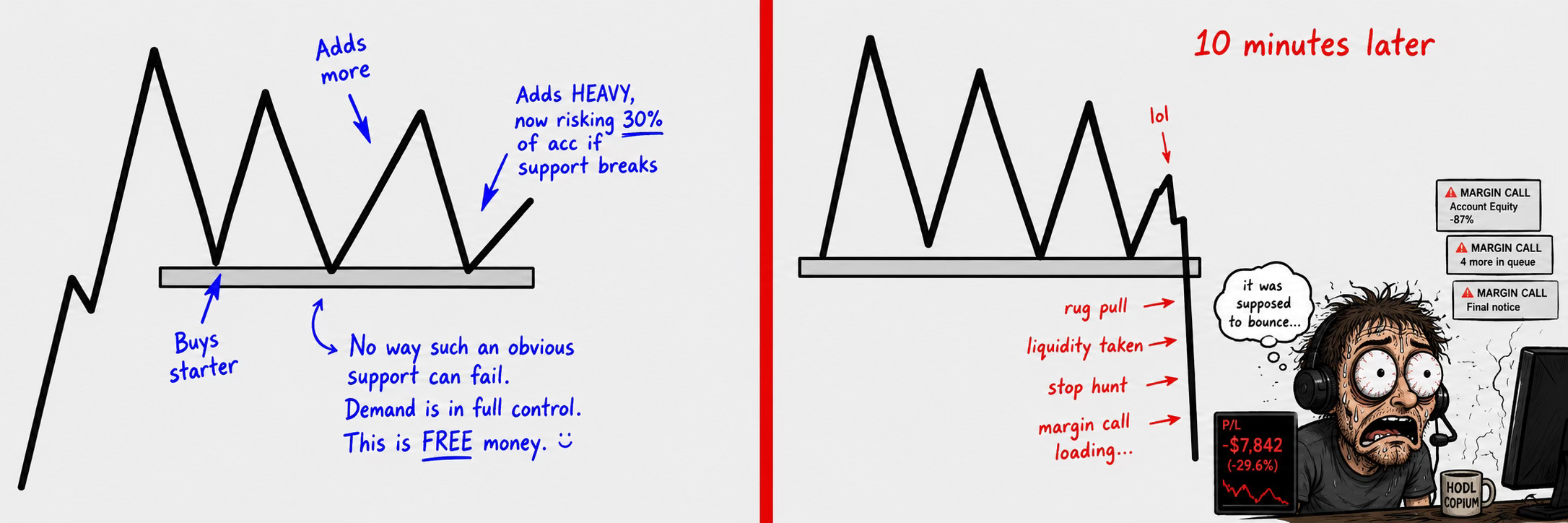

Imagine a trader with a $10,000 account who takes a position large enough that a 30% move against them would create a $3,000 loss. In small-cap stocks, a 30% move within 15 minutes is not unusual, so this kind of sizing immediately puts the trader in a dangerous position.

If the stock breaks a key support level, that trader becomes highly vulnerable to liquidity raids and stop-hunting behavior. Their position is large enough that even a normal small-cap shakeout can trigger panic, emotional decision-making, or a forced exit.

The risk is not just being wrong. The risk is being right eventually, but sized so aggressively that the trader gets shaken out before the trade has time to work.

High leverage, oversized positions, and lack of experience all increase psychological pressure. That pressure often leads to panic selling, chasing exits, or placing obvious stops where larger players can easily target liquidity.

Even experienced traders can fall into the same trap when they have too much conviction, size too heavily, or expect the price to move in their favor too quickly. When price stalls or moves against them first, they become part of the liquidity that stronger players are trying to extract.

We know the average retail trader is usually undercapitalized, overleveraged, and often risking too much of their account on a single idea. That combination is exactly what makes them vulnerable to liquidity hunting, emotional stop-outs, and market maker games.

When a trader is oversized, inexperienced, and emotionally tilted, they become much easier to manipulate. Revenge trading, bad sizing, and a poor read on the stock create the perfect psychological setup for getting trapped.

Here’s a crude real-life example.

Imagine you are calm, collected, and thinking clearly. Someone tries to provoke you. If you are naturally analytical and not looking for conflict, you probably de-escalate. You do not take the bait. You do not feed the situation.

Now imagine the opposite. You are already having a terrible day, you are agitated, your heart rate is elevated, and you are emotionally charged. In that state, you are much more likely to react. The provocative person has already won because they pulled you into their game. You got triggered, and now you are responding on their terms.

That is similar to how the market gets traders, especially when they start revenge trading right from the open.

Price action traps work the same way. The setup is not just technical. It is psychological. If you are emotionally unstable, oversized, or desperate to make back losses, the market has a much easier time pulling you into bad decisions.

That is why I rarely trade when my mindset is not stable. On those days, I either sit out or size down significantly. This is especially important when trading highly manipulative small-cap names. If you are stepping into that kind of battlefield, you need to understand the dynamics first and only participate when your mind is clear.

Stop assuming that the order flow on a ticker is mainly being created by ordinary traders like you.

A large portion of volume and order flow is artificial or engineered. Think about it like walking into a casino. Do you believe the casino exists because of the people sitting at the tables that day? Or does the casino exist because an operator built the environment first: the building, the staff, the games, the systems, the incentives, and the odds that favor the house?

The answer is that both can be true to some extent.

Five friends can get together and run a small poker game among themselves. That is a small, low-liquidity version of a casino environment. But that is not where serious money is made at scale. A five-person poker table does not scale. A real casino does.

To scale, you need infrastructure. You need capital. You need a house. You need staff. You need many games running at once. Most importantly, you need a constant rotation of players coming in and out so transactions keep happening.

That is the better way to think about markets.

When you enter the market, do not focus only on the other players sitting at the table. First understand that you are entering an engineered environment. The house is designed to win over time because the house controls the structure, the liquidity, the incentives, and the games being offered.

Modern markets operate in a similar way. That is why traders should stop obsessing over “pump groups” as the main driver and start paying more attention to the casino itself: the larger operators, market makers, liquidity providers, and entities that structure the game.

Once you understand that the house is built to win on average, you should not walk in overly excited, thinking easy money is waiting for you. You should be cautious, because the environment is not built for your benefit. It is built to extract from participants who do not understand the game.

That is where many beginner traders get trapped. They enter the market thinking they discovered some hidden money machine. Because few people around them trade seriously, they assume trading must be some secret shortcut to fast wealth.

I thought the same thing in the beginning too.

And looking back, that was exactly the wrong mindset.

Here is a rough framework for how a heavily engineered small-cap squeeze could potentially play out.

It may begin in pre-market with aggressive buying that absorbs a large portion of the float. This forces prior holders to start selling into the move, giving the dominant player control over more inventory and helping them shape the tape early.

Once the regular session opens, the game becomes more tactical. The operator may create repeated traps: spike the stock to pull in longs, dump it under key lows to bait shorts, then reverse it again to force covers and create more liquidity. The goal is to keep activity moving, not always price itself. They may buy some, sell some, and continuously create enough motion on the tape to attract participation from both sides.

Eventually, if the tape starts drying up and new longs or shorts are no longer coming in aggressively, the operator may begin preparing for the next phase. In some cases, they may build a larger short hedge. This does not always happen, but when it does, it often requires price to consolidate for several minutes so the position can be built without being too obvious.

In my view, the names where they choose to hedge short are likely the ones where they control a significant portion of the float but cannot unload that inventory quickly enough into natural long demand. If the tape is too slow and there are not enough buyers to absorb their shares, building a short hedge gives them protection before they begin the controlled dump. This is where certain consolidation setups can become useful, because they allow time to build that hedge before the breakdown.

From there, the final stage is unloading the long inventory while gradually covering the short position into the decline.

To run a game like this, several things are required.

First, you need enormous capital and buying power. This is far beyond what most retail traders have, and even beyond what many prop traders can access. You need enough size to influence the float, control liquidity, and keep the tape active.

Second, you need access to borrow inventory and strong market infrastructure. The players running these moves need access to shares before most others do, so they are not the ones left trapped when the setup turns. This is a key point. Massive small-cap squeezes have become more common as shorting access has expanded across institutions and market participants. That is not a coincidence.

If the dominant player has access to a large borrow pool, they can push a stock much higher, knowing they have the ability to hedge short later. This helps explain why some squeezes can get so extreme. They are not necessarily squeezing a ticker just to chase one small short seller. They may be squeezing it because they can later hedge their long inventory near the top and profit from the collapse.

Third, they need a deep understanding of price-action psychology. They need to know how to create traps, force emotional reactions, trigger stops, bait longs, bait shorts, and paint the chart in a way that makes traders act predictably.

There is only so much that can happen during a normal trading session. Time, liquidity, and price movement all create limits. That is why these patterns repeat. Manipulation does not have infinite creativity. The structure changes from ticker to ticker, but the mechanics often rhyme because the same psychological pressure points are being used.

In simple terms, the people designing these moves understand how to put predatory tactics directly into the chart.

When all of those ingredients are present, the process becomes easier to understand.

Large capital can force the stock higher through relentless buy-sell-buy-sell activity, creating the appearance of major demand. The tape looks active, the price looks strong, and long-biased traders start believing something real is happening. But in many cases, the liquidity itself is part of the illusion.

You have probably seen this before: a small-cap stock trades massive volume, breaks high of day, looks like it is about to go nuclear, and then suddenly dies minutes later. That is not random. That is part of the game.

Borrow access and shorting capability allow the same players to flip the script once they no longer want to push the stock higher. In some cases, they need to go short because they were the main buyer near the top. If they simply start selling their long inventory with no hedge, the bid can disappear instantly and the move can collapse against them too quickly.

A short hedge lets them crush the bid while still holding long inventory. It reduces the damage from the top down and allows the controlling party to manage the unwind more efficiently.

The traps created along the way are what provide the liquidity. Longs get sucked into breakout attempts. Shorts get baited under lows. Stops get triggered. Traders get emotionally forced into bad exits.

That is liquidity hunting.

Or put another way: it is an international wire transfer from traders who never agreed to send the money.

hey i noticed this on friday during the ceasefire candle was in shorts and almost panic sold due to news but held, if the volume is fake and big buyers paint the chart then as a new trader isnt it better to turn off volume to avoid panic entry/selling or do i keep it on to spot traps